High food prices add to Sub-Saharan Africa's economic woes

- The war in Ukraine is having a major impact on Sub-Saharan Africa (SSA). The increase in food prices aggravates food insecurity due to climate change and conflict. Inflation is increasing sharply and resulting in monetary tightening across the region. Many countries have high financing needs and face a worsening of financing conditions.

- Economic growth is slowing in SSA due to the high cost of living, domestic and external monetary tightening and the global economic slowdown. Growth figures vary across the region, depending on the economic structure and domestic issues.

- The worsening of socio-economic conditions could undermine political and social stability in the most volatile countries. In the past year, people took to the streets to demonstrate against the high cost of living in several countries. In addition, political instability has increased in some countries, due, for instance, to military coups.

- Years of high budget deficits have pushed public debt to levels not seen in years. The higher interest rates, both domestic and external, and the stronger dollar increase debt vulnerabilities. Therefore, the risk of debt restructuring has increased.

- Risks for the outlook are on the downside. The region’s outlook is vulnerable to a prolonged war in Ukraine, climate change and the global economic slowdown.

Just as it was recovering from the pandemic, another external shock hit the Sub-Saharan African region. The war in Ukraine triggered a steep rise in food and fuel prices, pushing inflation in African countries higher, and resulting in increased volatility on the international capital market. Both have, although in varying ways, a major impact on several African countries. In a region where food accounts for a larger share of spending than in most developed countries, the consequences of the sharp increase in food prices are dire. This comes at a bad time as many countries in the region already faced food insecurity due to conflict (Ethiopia) and drought (Horn of Africa). According to the World Bank, SSA has the world’s highest share of food-insecure people (more than 100 million in 34 countries). In combination with higher fuel prices, the cost of living has risen sharply this year in many African countries and will have a negative impact on the economy. The poverty rate will deteriorate in the most vulnerable countries. Unlike developed countries, many African governments lack the room to support their population, as the impact of the Covid-19 pandemic is still visible in government finances. Overall, budget deficits are still high and debt levels have risen sharply in recent years. As many still issue subsidies, the increasing prices for food and fuel will also raise the subsidy bill and put a further strain on fiscal balances.

At the same time, the increased volatility on the international capital market and more aggressive monetary tightening in the US and the eurozone than expected before the war caused a deterioration of the financing conditions. Faced with high financing needs, risk premiums for frontier markets such as Ghana, Senegal and Kenya have jumped to levels not seen in years, and access to the international capital market has in fact vanished for them. In previous years, several African countries had issued bonds, benefitting from low interest rates and the search for yield. Since the war in Ukraine, only Angola, South Africa and Nigeria have issued a Eurobond. No longer being able to access the international capital market and in need of financing, many countries have opted for an IMF program. Over half of the African countries have been or are negotiating with the IMF. According to the IMF, it has been supporting SSA countries with close to USD 50 billion since the beginning of the pandemic. During the pandemic, the IMF provided financial support through new rapid financing facilities and augmented existing financing programmes to help the countries combat the shock. To address the current food crisis, the IMF is introducing a new facility, the Food Shock Window. In addition, the World Bank has initiated many projects to support the agricultural sector and protect the most vulnerable.

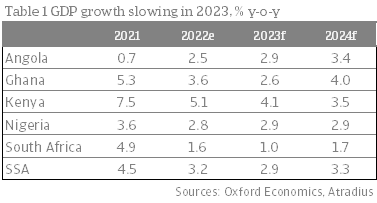

Because of higher inflation, increasing interest rates and a global economic slowdown, economic growth in SSA will decelerate to 3.2% in 2022, compared to 4.5% in 2021. As we expect the current challenges to remain in the coming year, economic growth will turn out slightly lower in 2023 at 2.9%.

Rising food prices have major impact

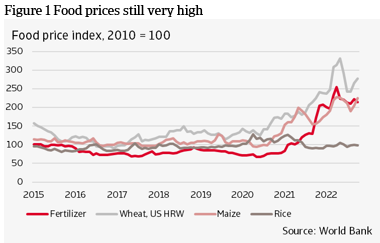

Global food prices have risen sharply since the Russian invasion in Ukraine. In particular, the price of wheat has skyrocketed because Russia and Ukraine are the main wheat exporters. Wheat is, in addition to maize and rice, a staple foodstuff in SSA. Many SSA countries are dependent on imports for their staple foods, especially when local harvests fail to keep up with domestic consumption. SSA imports approximately 85% of its wheat.

Some of the world’s largest increases in food prices are seen in Africa. Because of the high import dependency, the pass-through from global prices to local food prices is significant. Food inflation was above 30% y-o-y in Ethiopia, Ghana and Rwanda in October this year. Many others also record high food inflation figures. Food prices have already shown an upward trend in SSA since the beginning of 2021. Not only global developments were responsible for this. Domestic factors like the share of staples in food consumption, net import dependence and exchange rate depreciation also contributed to high food inflation. In addition, the worst drought in 40 years hit East Africa, and conflicts in Nigeria and Ethiopia had a negative impact on their agriculture sector. The war in Ukraine has exacerbated this trend.

Price of fertilizer will keep food prices high

High input costs can keep food prices elevated and aggravate food insecurity. According to the World Bank, food prices could be subject to more upward pressure if energy and fertilizer prices remain high in 2023 and 2024. The price of fertilizer has risen sharply since the beginning of 2021 due to the increase in energy prices. Fertilizer is the most energy intensive commodity group, according to the World Bank. Due to the high energy prices and/or unavailability of feedstock, several companies, especially in Europe, have temporarily closed their factories. The market for fertilizer is tight due to restrictions on fertilizer exports from the Black Sea region, sanctions on exports from Belarus and China’s fertilizer export ban.

Inflation increases across the region

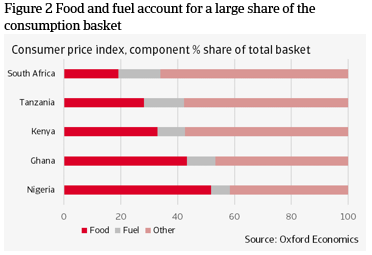

Higher food prices are impacting strongly on inflation in SSA because in most countries the share of food in the consumption basket is above 20%, with countries like Ethiopia, Zambia, Nigeria and Senegal even having a share of around 50%. Only Botswana, Seychelles and South Africa have a share of less than 20%. It is not only food that has a large share in the consumption basket; fuel also accounts for an important part. Most SSA countries are dependent on refined fuel imports. Even countries that export oil feel the burden of a high oil price because of the import dependency of refined fuel (Nigeria).

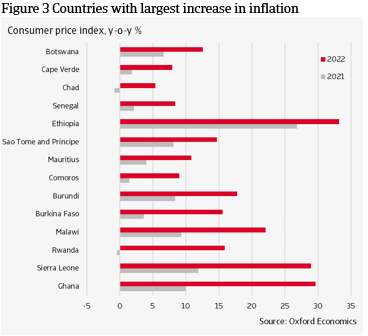

The sharp increase in food and fuel prices has resulted in high inflation figures across the region. We see considerably higher inflation for instance in Ghana, Burkina Faso and Rwanda. It is not only the higher food and fuel prices that contribute to this. The war in Ukraine has exacerbated existing inflationary pressures due to currency depreciation (Zambia, Ghana), monetary financing (Ghana) and conflicts that have resulted in food shortages (Nigeria, Burkina Faso, Ethiopia).

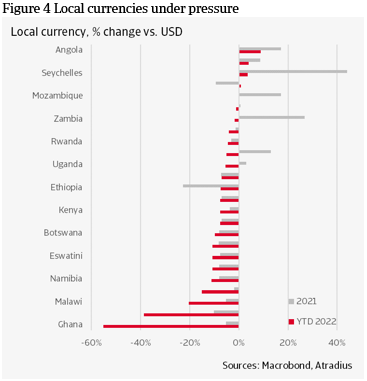

Many African countries have tightened monetary policy to contain inflation and to ease pressure on the exchange rate. Year to date, most currencies across Africa have depreciated against the dollar, especially since the war in Ukraine. A number are suffering significantly where external shocks have exacerbated domestic issues (e.g., Ghana). Due to decreasing external demand, global monetary tightening and relatively high domestic inflation currencies of, for instance, Nigeria, South Africa and Kenya will remain under downward pressure. Consequently, further monetary tightening across Africa is expected in 2023, especially in Ghana, South Africa and Ethiopia.

Heightened political risks

The rising cost of living undermines political and social stability. Already in countries like Nigeria, Senegal, Ghana, people have taken to the streets to protest against the higher costs. Particularly in combination with high (youth) unemployment, the high cost of living will lead to further social unrest. This poses a threat to political stability, especially in already volatile countries. Political instability and conflict have increased in recent years. In the Sahel region, the security situation has deteriorated due to increased activity of terrorist groups. Mali, in particular, has seen a sharp increase in terrorist attacks, which have spread to Niger and Burkina Faso. From there the threat has recently spread into the northern areas of coastal countries Benin, Cote d’Ivoire and Togo - countries that were relatively unaffected by terrorist threats so far. In West Africa, there have been military coups in Mali, Guinea and Burkina Faso and attempted coups in Niger and Guinea-Bissau, raising the fear of contagion. In Ethiopia, a roadmap to peace was agreed in November 2022 after two years of clashes. Several countries are due to hold elections in 2023 that could spark unrest, especially in the current environment of worsening social economic conditions. Most watched are the upcoming elections in Nigeria, Ethiopia and South Africa.

Increasing interest rates jeopardize debt sustainability

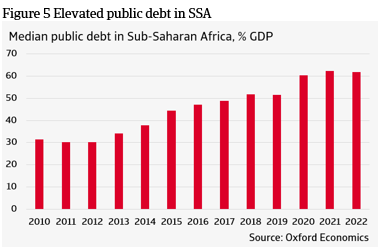

Higher interest rates, both domestic and external, and the stronger dollar increase debt vulnerabilities across the region. Public debt is approaching levels not seen since the early 2000’s when many countries benefitted from the debt relief of the Heavily Indebted Poor Countries Initiative and the Multilateral Debt Relief Initiative of the IMF and World Bank. Public debt has increased sharply since 2014 due to high public investment and spending. A drop in oil prices caused a steep rise in public debt among oil exporting countries (Angola, Gabon) and more recently, the Covid19-pandemic hit African government finances. Across the region, governments increased spending on social services, and revenues dropped, resulting in wide budget deficits and growing public debt. In 2022 the median public debt will hover around the same level as in 2021. However, some countries have an even higher debt level.

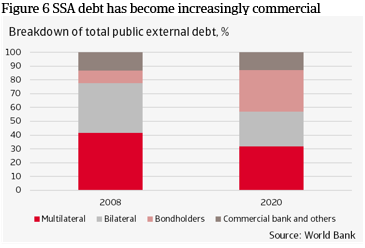

Before the war in Ukraine, many African countries benefitted from the low global interest rate and the search for yield. Countries like Kenya, Ghana and Senegal issued bonds that yielded lower interest rates than their domestic bonds, lowering the debt servicing costs - initially, at least. As some countries have increased the use of commercial external debt at the expense of long term, multilateral debt with low interest rates, debt servicing costs have increased in recent years. Looking at the debt structure, this change was considerable over the years. The share of bondholders has increased sharply at the expense of bilateral and multilateral creditors. In addition, non-traditional bilateral creditors like China have increasingly replaced traditional bilateral creditors.

Risk of debt restructuring increasing

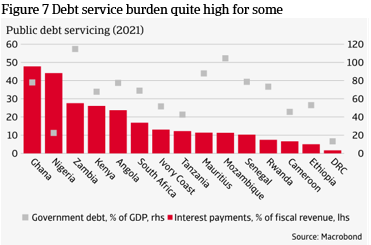

Due to the elevated debt levels, more governments face a high debt service-to-revenues ratio, limiting the room to invest or spend on social services. For Ghana, Nigeria, Zambia and Kenya, the debt servicing burden eats into a large share of their revenues. With respect to Nigeria, this seems remarkable looking at the low level of public debt. However, due to the extremely low government revenues, debt sustainability is a concern.

More challengingly, with borrowing costs rising and interest for African debt fading it could prove difficult for some countries to service and roll over large amounts of debt. This will be most evident in 2024 when large amounts of debt repayments fall due. Currently, most African countries have lost access to the international capital markets, and for some, sovereign spreads hover above 1,000 basis points indicating future financial distress.

During the pandemic, the G20 provided debt relief to the low-income countries through the suspension of debt service payments to official creditors. This initiative, the Debt Service Suspension Initiative (DSSI) helped the countries to support the most vulnerable households and provided room to increase spending on health. Around 30 countries, including Kenya, Senegal and Angola, participated in this initiative. It was, however, mainly a short-term liquidity solution; it ended in December 2021 and participating countries need to start repaying the suspended debt service payments next year.

Looking at the elevated debt levels and the increasing risk of sovereign defaults, a structural solution is necessary. This could mean that more African countries will join the G20 Common Framework. This initiative provides debt restructuring in cases of unsustainable public debt. All creditors, including private creditors, participate in this framework. So far, only Zambia, Ethiopia and Chad are in the process of restructuring their public debt under this framework. Progress is, however, very slow with each country having their own issues. Due to the protracted nature and complexity of the process, other countries are reluctant to participate in the Common Framework. For countries with one particular creditor, in most cases China, a bilateral restructuring might then be more efficient than one with all creditors under the same conditions. Angola took this route in 2020 when it restructured part of its Chinese debt. This would be especially relevant for Kenya, which according to recent media reports, may already have defaulted on Chinese loans that funded its railway project.

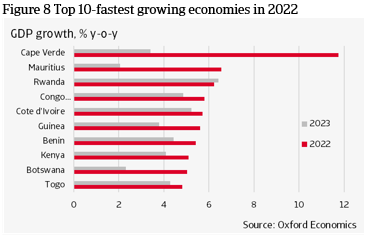

Varying growth rates across SSA

Growth rates in the region vary widely. The small-island, tourism-dependent economies of Mauritius and Cape Verde, hit hard by the pandemic, show a strong economic recovery in 2022. Tourism to these destinations is rebounding as they have removed their Covid-19-restrictions and both have successfully vaccinated a relatively large percentage of the population. In 2023, economic growth will slow significantly, as tourism will be negatively impacted by the global economic slowdown.

Diversified economies among the front-runners

Among the fastest growing countries in 2022 are mainly the ones that have a diversified economy and a reasonable business environment. Cote d’Ivoire, Rwanda and Benin also fared relatively well throughout the pandemic due to high public investment. Investments in infrastructure and reform implementation are among the measures supporting economic growth in these countries. Despite some headwinds, Kenya is one of the top-performing countries in 2022. However, economic growth is decelerating due to highly charged presidential elections in August, a delay of IMF funding, a sharp increase in inflation and concerns about debt sustainability. On the positive side, there was minimal violence before and during the elections. In addition, investment and social spending increased, thereby providing support to the economy. In contrast, in Ghana the situation looks dire. Economic growth decelerates this year and next year. Sentiment towards Ghana deteriorated amid concerns about debt sustainability and several rating downgrades by external rating agencies. The currency depreciated by more than 50% this year against the dollar, inflation is high and the central bank of Ghana raised the interest rate sharply. Faced with an economic crisis and in need of debt restructuring, Ghana follows the path of many other African countries in recent years and turned to the IMF for financial support.

Metal-exporting countries benefit in 2022

With a few exceptions, commodity-exporting countries are also doing well. Botswana, Congo Kinshasa and Guinea benefit from the increasing demand and high prices for iron ore, copper and diamonds. The higher prices result in ramped-up production and exports. Overall, commodity-exporting countries are doing fine, but not as well as last year when commodity prices increased sharply. In 2021 prices for commodities rose thanks to the global economic recovery after the pandemic, increased demand from China and some supply factors. Commodity prices initially increased further due to the war in Ukraine. However, more recently, the global economic slowdown and concerns about the Chinese economy have led to a decline in some commodity prices, especially for metals. Commodity prices will remain volatile and are expected to ease further next year in the wake of the global economic slowdown. Nevertheless, commodity prices will remain elevated by historical standards and provide support to the commodity-exporting countries. That said, for most commodity exporting countries growth will decelerate from the highs of this year.

Largest economies in the region lag

Despite the recent decline, prices for oil and gas remain at a high level. Therefore, it is surprising that oil-exporting countries are not in the top-10 fastest growing SSA countries this year. Growth in oil-exporting and largest economy in SSA, Nigeria, has decelerated to 2.8% in 2022 due to several domestic factors. Most important is the decrease in oil production. Oil supply disruptions, theft and sabotage have resulted in the lowest production figure in four decades. Nigeria has thereby missed out on profiting from the high oil prices. In addition, high inflation (2022: 18.7%), high unemployment and a tight forex situation are among the factors contributing to the economic slowdown. Besides these economic factors, security issues and the coming elections in February 2023 will keep economic growth subdued next year. Another oil-exporting country, Angola, is showing moderate economic growth this year after five years of recession. The rise in oil production is providing support to the economy. However, high inflation, high unemployment and high interest rates are constraining domestic demand.

Despite the support from high commodity prices, the second largest economy in the region, South Africa, is one of the growth laggards in SSA. Problems at state utility Eskom have resulted in scheduled power outages, which are undermining the economy. Besides these, high (youth) unemployment, high inflation and monetary tightening constrain domestic demand. These factors will also contribute to a subdued economic growth of 1.0% in 2023, making the country the growth laggard in SSA.

Resource abundance attracting foreign interest

Many African countries have abundant resources that have drawn international interest. Owing to the sanctions on Russia, there is increasing interest in African oil and gas. Among European countries, there is a particular need to replace Russian oil and gas and diversify energy imports. Germany, especially, is looking for alternatives to its Russian gas dependency and is increasingly looking to Africa. Countries like Mozambique, Tanzania, and Nigeria have abundant gas reserves. In the short term, this will provide support to the energy sector on the African continent and could lead to increased investment in countries like Angola, Nigeria and Ghana. However, the energy transition and decarbonisation of the global economy mean that these countries need to diversify their economies and become less dependent on oil and gas for their growth.

Many African countries have enormous potential for renewable energy and could become major exporters of green energy and develop into a hub for green-powered production. There is also interest in financing several African initiatives to produce hydrogen energy for exports to Europe. For instance, Namibia wants to develop a mega green hydrogen project. In addition, many countries have an abundance of the minerals used for renewables. International competition is increasing to secure long-term access to strategically important industrial inputs. Copper, cobalt, iron ore and manganese are among the important inputs for the energy transition and are present in abundance in various African countries. Around 30% of the world’s mineral reserves are in Africa. The largest reserves of cobalt, diamonds, platinum and uranium are in Africa. Mining in, for instance, Botswana, Congo Kinshasa, Namibia, South Africa, Tanzania and Zambia could expect increasing foreign interest.

Troubling outlook ahead

Risks for SSA’s growth outlook are mainly on the downside. A prolonged Ukrainian war will keep the import bill high for those countries dependent on food and fuel imports, putting fiscal and external balances under further strain. To counteract high inflation, central banks are raising interest rates, which will constrain domestic demand. Higher interest rates, both domestic and globally, will increase financing costs and hit the most indebted nations. This raises the risk that some might need debt restructuring. Countries most at risk are Ghana, Nigeria and Kenya, with indications that Ghana is already taking steps towards debt restructuring. Tighter government finances alongside the high cost of living also increase the likelihood of political instability and social unrest.

The high dependency on agriculture makes the region particularly vulnerable to climate change. Several countries have already experienced the negative impact of climate change on their agricultural sector in 2022. Adverse weather conditions are also a real possibility next year, which would worsen the food crisis and public finances. Without sufficient access to financing for effective adaptation and mitigation measures, many African countries are trapped in a vicious circle increasing their exposure to climate shocks. A solution to tackle both the climate crisis and the debt crisis at once could be the so-called debt-for-climate swaps, but such financial instruments are not yet widespread enough to significantly reduce these risks in 2023.

Finally, the region is also vulnerable to the global economic slowdown. Most worrying for Africa is the Chinese economic slowdown, as for many African countries, China is an important export destination. The global economic slowdown will weigh on commodity prices and weaken external demand for African commodities.

Afke Zeilstra, senior economist

afke.zeilstra@atradius.com

+31 (0)20 553 2873