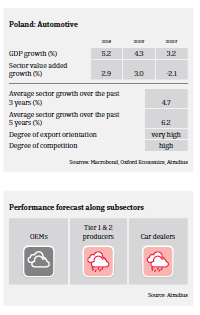

Insolvencies are expected to increase by about 3% in the coming 12 months, mainly affecting car dealers, car part distributors and Tier 2 suppliers.

- For both OEMs and suppliers the burden of innovation in order to adjust to new emission standards is high, while the industry has to cope with declining demand. According to OICA, Poland´s automotive production decreased 4.4% year-on-year in 2018, and the decline continued in 2019 (down 3.5% in Q1 of 2019). Global economic uncertainties weigh on sector performance (55% of Polish automotive production value was exported in 2018).

- Competition is very high in the industry with price wars and consolidation pressures, particularly visible in the car parts distribution and car dealers segments. Profit margins in the automotive sector have steadily decreased since 2015 due to wage pressures and increased commodity prices. Margin deterioration will likely continue in the coming months, reinforced by rising R&D expenses necessary for electric vehicle development and adjustment to new emission requirements. Effective logistics and IT solutions in distribution as well as proper stock management are key success factors for businesses if they are to sustain their margins.

- Payment duration in the automotive sector is about 115 days, on average, in the car parts & accessoires production segment and about 75 days in the distribution subsector. We recorded a substantial increase in the number of non-payment notifications and credit insurance claims over the last 18 months.

- Given the current issues (decreasing production output domestically and in the EU, looming uncertainty about Brexit and trade wars, technological adjustments related to fuel emission reduction/shift to electric vehicles) we expect payment delays to rise further. Insolvencies are expected to increase by about 3% in the coming 12 months, mainly affecting car dealers, car part distributors and Tier 2 suppliers.

- In the coming 2-3 years we expect the shift to e-mobility to increase the credit risk for Tier 2 suppliers that cannot cope with changing demand, leading to higher insolvency levels. At the same time many Polish suppliers are rather resilient as they are part of large international groups. Some locally-owned suppliers recorded higher margins than in other sectors over the last couple of years and are well capitalized. It remains to be seen if financial buffers are high enough to adapt the product range.

- Our underwriting stance is generally neutral to restrictive for the sector. We increasingly consider whether manufacturers and suppliers are bound to innovation (electric/hybrid cars) or are overly dependent on diesel vehicles, and if they have the financial strenghth to invest in new technologies.

- We are more cautious with smaller Tier 2 companies due to heavy competition in this segment and lower bargaining power. The same accounts for distributors of car parts and tyres, as this subsector is characterized by low margins, intense competition and slow stock turnover.

- Due to the high dependence on exports, a hard Brexit and/or any imposition of US import tariffs would have an adverse impact on the Polish automotive sector, especially for Tier 1 and Tier 2 businesses.

Kapcsolódó dokumentumok

Market Monitor Automotive 2019

1.19MB PDF