Atradius Atrium

Lépjen be az új online szerződéskezelő rendszerbe, amely segítségével egy helyen érheti el az Atradius összes online alkalmazását.

Magyarország

Magyarország

Ausztrália

Ausztrália

Ausztria

Ausztria

Belgium

Belgium

Brazil

Brazil

Bulgária

Bulgária

Cseh Köztársaság

Cseh Köztársaság

Dánia

Dánia

Egyesült Államok

Egyesült Államok

Egyesült Arab Emírségek

Egyesült Arab Emírségek

Egyesült Királyság

Egyesült Királyság

Finnország

Finnország

Franciaország

Franciaország

Görögország

Görögország

Hollandia

Hollandia

Hongkong

Hongkong

India

India

Írország

Írország

Japán

Japán

Kanada

Kanada

Kína

Kína

Lengyelország

Lengyelország

Litvánia

Magyarország

Litvánia

Magyarország

Mexikó

Mexikó

Németország

Németország

Norvégia

Norvégia

Olaszország

Olaszország

Portugal

Portugal

Románia

Románia

Spain

Spain

Svájc

Svájc

Svédország

Svédország

Szingapúr

Szingapúr

Szlovákia

Szlovákia

Szlovénia

Szlovénia

Törökország

Törökország

Új-Zéland

Új-Zéland

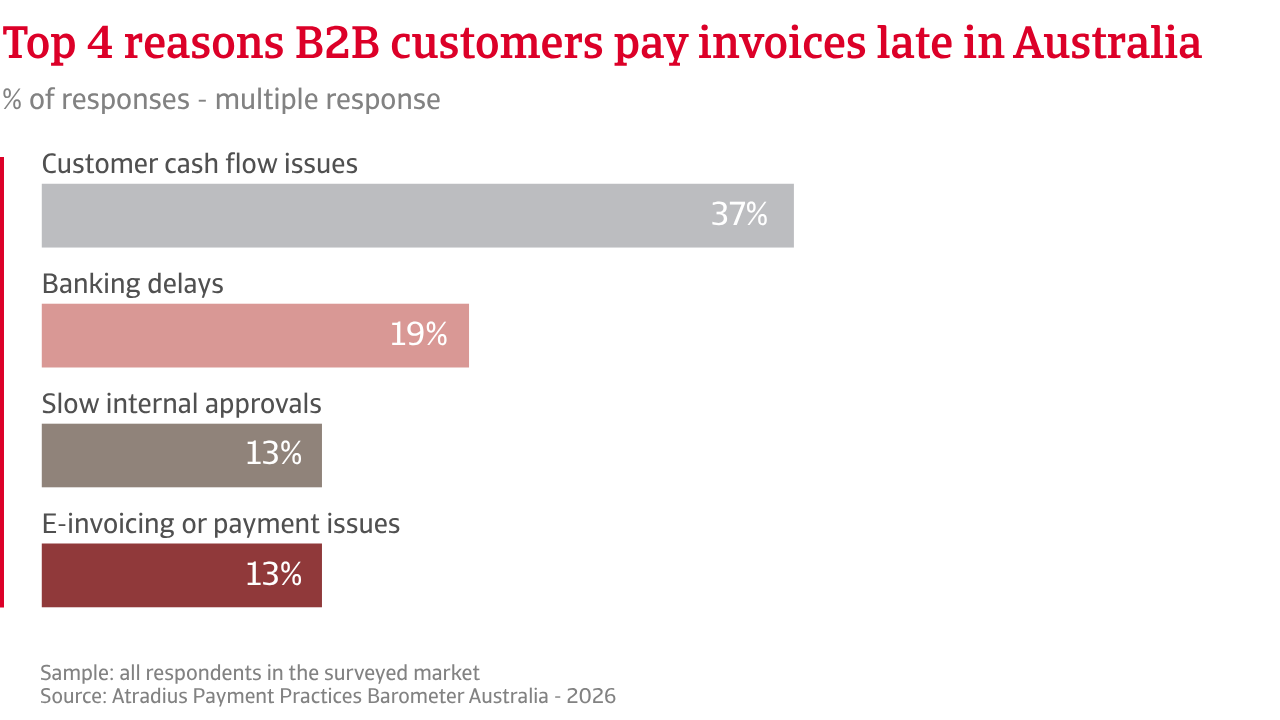

The economy is growing steadily as Australia enters the second quarter of 2026. However, uncertainty in global trade is expected to keep commodity prices contained and weigh on exports. Inflation remains above the central bank’s target, adding pressure on business costs. Interest rates are higher than in recent years, making borrowing more expensive. Access to finance has tightened as banks lend more cautiously, which may explain why companies in Australia increasingly rely on trade credit.

An upward trend in the use of trade credit is clear in B2B sales. Nearly 60% of transactions are made on terms, which means most B2B trade in Australia is now financed by suppliers. This increases exposure to customer payment risk until invoices are settled. When payments slow or customers request longer credit windows, it signals that cash-flow pressure is building. With borrowing expensive and the outlook uncertain, most companies in Australia have a lower appetite for risk and shorten payment terms to fewer than 30 days. Many also encourage quicker invoice settlement by offering discounts. Larger companies often pressure smaller suppliers to accept longer payment terms, so SMEs pay out faster but wait longer to be paid. This creates cash-flow pressure on smaller firms and can threaten their survival.

.2026-03-20-08-26-06.png)

Days Sales Outstanding (DSO) figures reveal that most B2B payments align with agreed terms. DSO averages three weeks, highest among large manufacturers. Fewer than one in five B2B invoices are overdue (18%), with bad debts contained for most businesses. However, this apparent payment discipline hides how stricter payment terms drive change in customer payment behaviour. As suppliers shorten terms to protect their cash flow, customers adjust how they manage theirs. Customers hold on to cash, review who to pay first, and prioritise suppliers they cannot afford to lose. Non-essential suppliers wait longer. This selective pattern does not show up in headline overdue rates, but points to pressure on cash flow. Real time credit data makes delays visible at once, allowing suppliers to tighten credit quickly. Firms that pay on time keep their credit lines open and protect their position in the supply chain.

Clear risk hotspots of uneven customer payment behaviour are emerging in specific business segments. These pockets of pressure sit beneath a steady headline picture and highlight where cash-flow strain may intensify. This is mainly in the construction sector, export-exposed industries, and SMEs under pressure from large buyers. Tax instalments add strain for many small and mid-sized companies and often trigger short periods of liquidity stress, during which payment risk can cluster. In response to this uneven payment pressure our survey shows that more businesses now view credit insurance as a strategic tool to protect cash flow and maintain financial stability.

Companies surveyed in Australia report growing concern about volatile global markets as the current geopolitical turmoil is disrupting trade flows significantly. Uncertainty about how the situation will evolve is adding further pressure on supply chains. Operating costs are expected to remain high, while transport reliability is likely to deteriorate further in the months ahead. Businesses anticipate that disruption along key trade routes will continue to lengthen delivery times and strain supply chains. These developments are likely to feed directly into operating expenses and influence how businesses prioritise payments. Many companies anticipate a clear shift in B2B payment behaviour during the coming months as customers assess their own liquidity and adjust payment schedules accordingly.

.2026-03-24-08-11-55.png)

Rising transport and energy costs are expected to further tighten liquidity across a wide range of sectors; prompting businesses to conserve cash, reassess budgets, and prioritise payments to key suppliers. Selective payment practices are becoming increasingly common as companies safeguard working capital and maintain operational resilience. This behaviour is most evident in sectors already exposed to elevated input costs and limited financial flexibility. It signals mounting strain in areas of the economy with little resilience. Profit margins are expected to come under sustained pressure.

Current evidence indicates that the sharpest margin compression will be experienced across several areas. These include fuel-intensive sectors, construction, export‑oriented industries, transport and logistics, retail and consumer goods supply chains, and smaller firms reliant on a small number of large customers. Higher freight charges, rising energy costs, and slower payments from clients will weigh directly on returns, reducing available capital for reinvestment and growth. Elevated interest rates compound the challenge by making borrowing more expensive, increasing financing costs, and widening the gap between businesses with strong cash discipline and those struggling with higher costs, rising inputs, and softer demand.

Economic slowdown remains a key concern for businesses in Australia, particularly in the context of volatile global markets and persistent inflationary pressures. Robust credit control, timely invoicing, and close monitoring of customer behaviour are essential to maintaining cash flow and operational stability. Firms must also plan for potential further disruptions to transport and energy markets, which could exacerbate liquidity constraints. Disciplined liquidity management, rigorous cost control, and proactive risk assessment will remain crucial for businesses to navigate an unpredictable operating landscape, ensuring they are prepared to respond effectively to continuously evolving economic and trading conditions.

For a full overview of the 2026 survey results for Australia, please download the report available in the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.