Atradius Atrium

Lépjen be az új online szerződéskezelő rendszerbe, amely segítségével egy helyen érheti el az Atradius összes online alkalmazását.

Magyarország

Magyarország

Ausztrália

Ausztrália

Ausztria

Ausztria

Belgium

Belgium

Brazil

Brazil

Bulgária

Bulgária

Cseh Köztársaság

Cseh Köztársaság

Dánia

Dánia

Egyesült Államok

Egyesült Államok

Egyesült Arab Emírségek

Egyesült Arab Emírségek

Egyesült Királyság

Egyesült Királyság

Finnország

Finnország

Franciaország

Franciaország

Görögország

Görögország

Hollandia

Hollandia

Hongkong

Hongkong

India

India

Írország

Írország

Japán

Japán

Kanada

Kanada

Kína

Kína

Lengyelország

Lengyelország

Litvánia

Magyarország

Litvánia

Magyarország

Mexikó

Mexikó

Németország

Németország

Norvégia

Norvégia

Olaszország

Olaszország

Portugal

Portugal

Románia

Románia

Spain

Spain

Svájc

Svájc

Svédország

Svédország

Szingapúr

Szingapúr

Szlovákia

Szlovákia

Szlovénia

Szlovénia

Törökország

Törökország

Új-Zéland

Új-Zéland

Survey findings among companies in Hong Kong show that nearly two in five business-to-business (B2B) sales are currently conducted on credit terms, below the regional average. This places Hong Kong among the lowest users of trade credit in Asia, with only China reporting a lower share, and levels broadly in line with Taiwan, while other markets report significantly higher use. Mid-sized services firms report extending credit more often than other segments. Compared with the regional trend, the more cautious approach to credit-based B2B trade shown by Hong Kong businesses reflects tighter risk management and a clear focus on limiting exposure to payment risk amid heightened uncertainty linked to global trade flows and geopolitics.

Business customers trading on credit with Hong Kong suppliers are offered payment terms of up to one or two months equally often. While two-month terms are more common than across the region, longer terms are less frequent in Hong Kong. Regional trend data indicate that Asian businesses lengthened payment terms in recent months to support B2B trade, a trend also observed in Hong Kong. Fewer businesses in Hong Kong than across Asia report stable B2B payment behaviour in recent months, highlighting a more volatile environment in the market than regionally. Where changes occurred, worsening outweighed improvement, and both were more often reported than across Asia.

Against this backdrop, 87% of companies in Hong Kong report delayed payments from B2B customers, translating into just under one third of invoices overdue at market level, below the regional average. Mid-sized and large firms in construction and services appear hardest hit. Trend data show that increases in overdue B2B invoices outweigh decreases among Hong Kong firms, in line with the regional trend but impacting a larger share of businesses in the market than regionally.

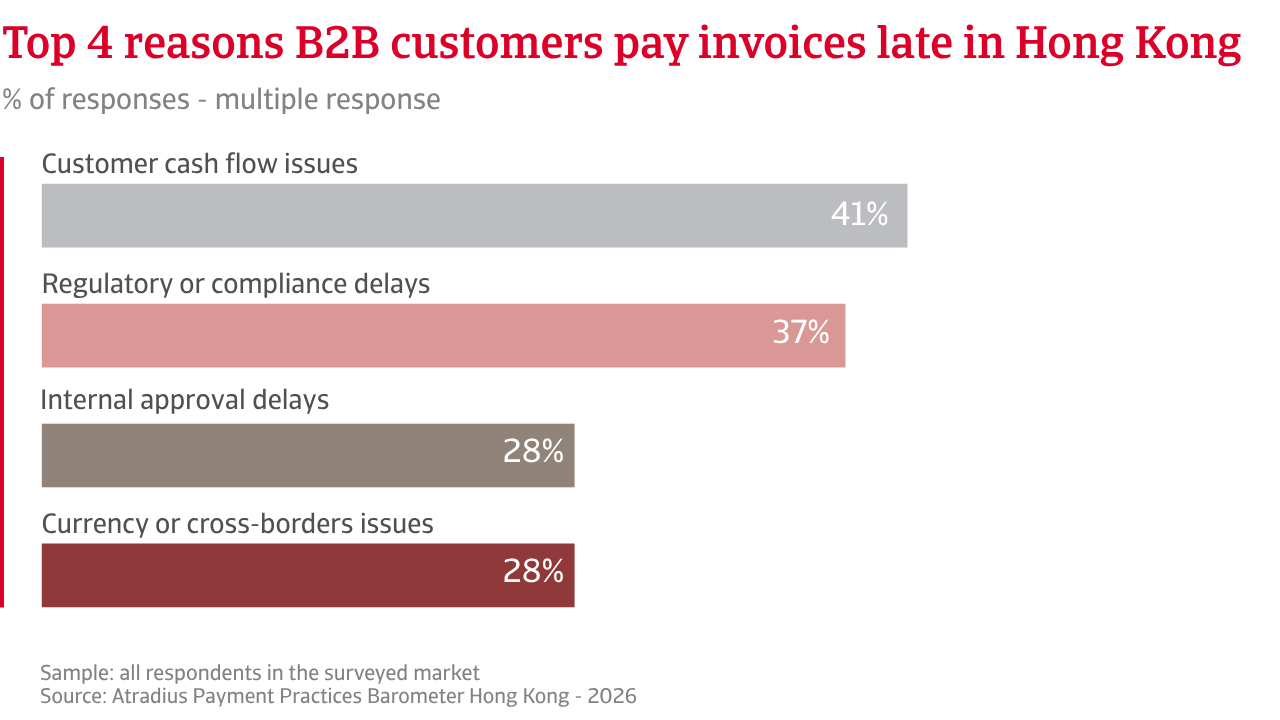

Based on survey responses, B2B customers in Hong Kong are less likely than those across the region to delay payments due to financial distress, with delays more often linked to payment processes, approval cycles and regulatory factors. As most payment terms in Hong Kong extend up to two months from invoicing, and delayed payments are typically settled within one month past due, the average collection period, reflected in Days Sales Outstanding (DSO), extends beyond agreed terms. This has shifted a large share of outstanding B2B receivables into a timeframe spanning two to three months, where cash remains tied up beyond agreed terms and exposed to payment risk.

Consistent with the deterioration in B2B payment behaviour in Hong Kong in recent months, this cluster has become a key risk area, with more receivables at risk of shifting into longer timeframes, where bad debt rises, increasing pressure on cash flow and working capital. Trend data support this dynamic, showing a stronger rise in bad debt write-offs than the regional average, with a greater concentration of losses in the 2% to 5% range than across the region. These levels can severely erode margins, as they translate directly into lost profit rather than reduced revenue. Write-off decisions in Hong Kong depend more on internal risk assessments and legal disputes, whereas across the region they are driven mainly by receivables ageing and customer insolvency.

For firms in Hong Kong, pressure on working capital means more businesses than across the region reporting higher funding costs, as borrowing to bridge liquidity gaps becomes more expensive and weighs on margins. At the same time, challenges in cash flow planning lead more companies to delay payments to suppliers, indicating a more defensive liquidity strategy. Firms tend to absorb working capital pressure internally, holding on to cash for longer and delaying outflows to manage liquidity. This makes timely cash collection the main constraint in the Hong Kong business environment.

As payment delays in Hong Kong appear to stem more from process delays that slow down payments, even when customers are able to pay, risk mitigation focuses on prevention, reducing exposure before it arises, through tighter terms and faster collections rather than risk transfer. While this approach supports control, rising bad debt and delayed collections expose its limits. Feedback from businesses using credit insurance highlights this gap. Beyond protecting against losses when delays turn into defaults, it helps stabilise cash flow and supports more confident trade, without the need to further tighten payment conditions.

Survey findings among companies in Hong Kong show that nearly two in five B2B sales are currently conducted on credit terms, below the regional average. This places Hong Kong among the lowest users of trade credit in Asia.

Hong Kong businesses have a different outlook compared with their regional peers on expectations for B2B payment behaviour in the coming months. Hong Kong stands out with a more cautious and uncertain outlook, as the share of firms expecting conditions to worsen is as high as those expecting improvement. This contrasts with the broader regional picture, where more businesses show stronger confidence in payment discipline. Fewer firms in Hong Kong expect stability, which suggests lower predictability and greater volatility in payment behaviour. This reflects broader signs of rising risk, as delays are highly likely to continue.

At the same time, expectations around insolvencies provide significant context. Across Asia, businesses expect either further increases or continued elevated levels, indicating ongoing pressure on corporate solvency. In Hong Kong, expectations are more concentrated, with most firms anticipating that insolvency levels will remain as current rather than rise further. This suggests that stress is already entrenched rather than building rapidly. As a result, the risk in Hong Kong appears less about sudden shocks and more about ongoing financial pressure. Persistent delays, combined with already elevated insolvency levels, are likely to continue weighing on cash flow, collections, and working capital, making risk management increasingly important.

Profit expectations reinforce this weaker outlook. Hong Kong firms show a more cautious and divided view than peers across Asia, with fewer expecting stability. This points to greater uncertainty around earnings. The underlying drivers are consistent. Slower payments, sustained insolvency pressure and higher funding costs are already affecting cash flow. This feeds directly into margin pressure, as delayed collections, higher financing costs, and rising bad debt weigh on profitability.

When asked about the main risks expected to impact B2B payment behaviour in the coming months, Hong Kong businesses clearly identify interest rate increases as the most significant factor, and at a much higher level than across the region. This points directly to rising funding costs and ongoing cost pressures linked to inflation. Cybersecurity and fraud risks also rank higher in Hong Kong than across Asia, highlighting growing operational challenges in managing receivables and payments. Macroeconomic risks, such as economic slowdown, carry less weight, suggesting that Hong Kong firms are more focused on financial execution and internal pressures than on external demand conditions. In this environment, cash flow protection, payment risk management, and maintaining financial flexibility remain the main priorities for Hong Kong companies in the months ahead.

For a full overview of the 2026 survey results for Hong Kong, please download the market specific report from the related documents section below. Insights into Asia are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.